Buying or selling a home always feels like a big leap, and for most people, it’s one of the biggest financial decisions they’ll ever make. There’s plenty of excitement as you move closer to getting those keys or handing them over. But with so many moving parts at the closing table, it’s easy to miss fees that add up fast—and both buyers and sellers can get blindsided.

Overlooked closing costs have a way of sneaking up just when you think you have every detail covered. Even small, missed charges can quickly ripple into your final numbers, affecting your plans and budget. Knowing which fees are most likely to get missed helps you avoid surprises and build real confidence when it’s time to sign.

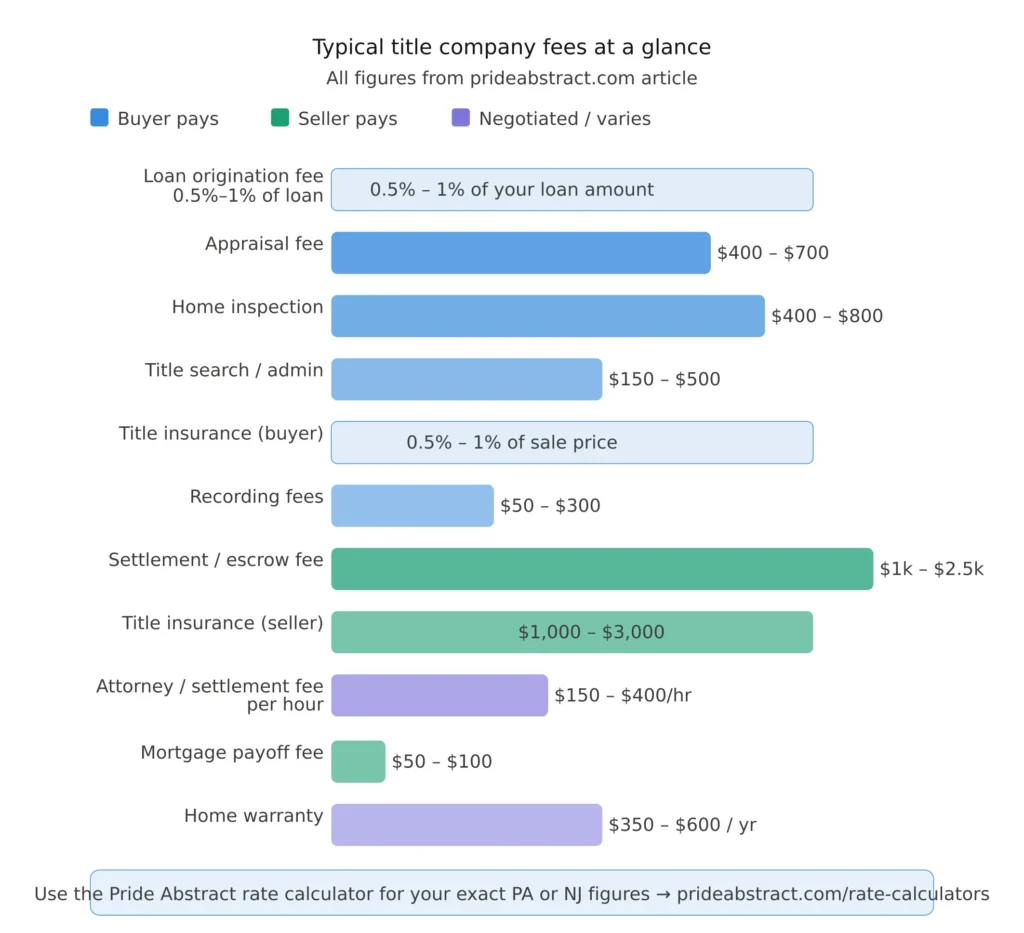

| Fee Type | Who Pays | Typical Cost (2026) |

|---|---|---|

| Loan Origination Fee | Buyer | 0.5% – 1% of loan amount |

| Appraisal Fee | Buyer | $400 – $700 |

| General Home Inspection | Buyer | $400 – $800 |

| Title Search / Admin Fee | Buyer | $150 – $500 |

| Owner’s Title Insurance | Buyer (recommended) | 0.5% – 1% of sale price |

| Lender’s Title Insurance | Buyer (required) | 0.5% – 1% of sale price |

| Recording Fees | Buyer | $50 – $300 |

| Transfer Taxes | Varies | Flat fee up to 1%+ of sale price |

| Settlement / Escrow Fee | Seller or split | $1,000 – $2,500 |

| Title Insurance (Seller Pays) | Seller (varies by state) | $1,000 – $3,000 |

| Attorney / Settlement Fee | Seller or buyer | $150 – $400 per hour |

| Mortgage Payoff Processing | Seller | $50 – $100 |

| Home Warranty (optional) | Negotiated | $350 – $600 per year |

Want to know your exact title company fees for your PA or NJ transaction?

Use our free rate calculator

Homebuyers often focus on the down payment and monthly mortgage. But the list of closing costs is much longer, with some fees hardly getting a mention until the very end. These overlooked expenses can catch anyone off guard—sometimes pushing budgets tighter than expected. Here’s where buyers get hit with fees they rarely spot in advance.

Lenders don’t process your mortgage for free. Most charge a loan origination fee to set up and begin processing your mortgage application. This covers paperwork, credit checks, and initial analysis of your loan worthiness. Underwriting fees go to the team responsible for taking a deep dive into your finances and making sure you qualify.

It’s common to forget these costs because they often blend into the bigger numbers. But when you’re borrowing, for example, $400,000, a 1% origination fee comes out to $4,000. That’s real money you’ll need available when you close.

When buying a home, getting the property professionally appraised is a must—lenders want a third-party confirmation of value. Beyond that, you’ll likely pay for a standard inspection. But many buyers don’t realize there are extra or specialized inspections that might become necessary, especially in older homes or certain regions.

Buyers routinely underestimate how these inspections add up. Missing one can introduce risk—getting all needed checks brings peace of mind, but at a real cost.

To protect yourself (and your lender) from ownership disputes, title insurance is required. What’s less obvious is you actually pay for two policies: one for the lender, and one optional but smart for yourself as the buyer.

Many buyers focus only on the insurance, totally missing the smaller title search charges for all the paperwork, legwork, and research behind the scenes. But those fees appear front and center on your closing documents. Want to know your exact cost before closing day? Use our title insurance calculator PA to get an instant rate estimate.

Every time a property changes hands, local governments need to update records. Recording fees and transfer taxes get paid to your state, county, or city. Price tags here swing wildly—what’s minor in one place could become a big chunk elsewhere.

It’s easy to overlook or underestimate these charges until the final numbers hit, especially if you’re buying in a region with higher real estate sales activity or state-specific tax rates.

This is where closing costs balloon for many buyers, because you prepay for future expenses upfront and fund your escrow account.

What might be included:

These costs sneak up because most buyers think only about their new monthly payment. At closing, hundreds or thousands more may be needed for escrow and prepaids, often pushing the grand total higher than expected.

Photo by Jakub Zerdzicki

Photo by Jakub Zerdzicki

For sellers, closing day should be the finish line—hand over the keys, collect your check, and move on. But in reality, a chunk of your sale price gets eaten up by closing costs you may not see coming. Even if you’re ready for the obvious ones, there’s always a chance for lesser-known fees to pop up last minute. Here’s what sellers routinely underestimate or miss entirely.

Break down how commissions are split, why rates vary regionally, and the impact of possibly paying both buyers’ and sellers’ agent commissions.

Agent commissions are usually the largest single fee sellers face. In most markets, the standard commission is 5% to 6% of your home’s final sale price. This gets split—typically right down the middle—between your agent and the buyer’s agent.

But here’s where things get tricky:

The bottom line: agent commissions rarely feel negotiable, but don’t be afraid to shop around. The numbers add up fast—a $400,000 sale could mean $24,000 in commissions alone.

Photo by Pavel Danilyuk

Photo by Pavel Danilyuk

Once you agree on a price, there’s still paperwork and legal work to get done, so the buyer can take clean ownership. Here’s where hidden title and transfer costs creep in:

It’s easy to miss these on your net sheet, but you’ll find them at the closing table, reducing your final payout.

Some states require a real estate attorney to review your sale, while others rely more on escrow or title companies. Either way, someone will get paid to verify everything goes by the book.

No one likes to see these charges at the end, but skimping on professional review is rarely worth the risk. Good legal and settlement help can save you from even bigger issues—think of it as an insurance policy for a clean sale.

You can’t hand over a clear title until the remaining balance on your mortgage is paid off. What many sellers forget is that there are costs—sometimes steep ones—attached:

All these pieces add up—and they’re usually non-negotiable. It’s smart to call your lender before listing to get payoff numbers, confirm penalties, and avoid ugly surprises right before closing.

At closing, both buyers and sellers often find extra charges hidden in the paperwork—fees that barely got a mention until now. These “nickel and dime” expenses can add up quickly and leave anyone frustrated if they’re not expected. These hidden fees can come from homeowner associations, utility companies, and even the title company’s admin desk. Knowing where to look is the only way to avoid a nasty surprise at closing.

If the home is part of a homeowners association (HOA), expect charges beyond the standard monthly or yearly dues. Both buyers and sellers can get hit with these, but how and when depends on the timing of the sale.

HOA-related closing costs can range from a few hundred dollars to several thousand if major repairs or upgrades are underway in the community.

Transferring utilities isn’t just about calling up the electric company. Both sides may owe small but stubborn fees that don’t always appear in the initial closing estimates.

These costs rarely break the bank, but they can push your final total higher if you miss them while planning.

Buried in closing statements are several “processing” fees nobody really talks about. These aren’t just for paperwork—they cover overnight shipping, wiring money, and copying documents to make the closing legit.

Photo by Jakub Zerdzicki

Photo by Jakub Zerdzicki

A quick glance at the settlement statement usually reveals a handful of these, but they’re easy to overlook. Reading every line, and asking what each admin-sounding charge means, makes a real difference in keeping closing costs in check.

Moving into a new home often comes with a mixed bag of emotions—excitement, anticipation, and sometimes a bit of sticker shock. Many buyers and sellers breathe a sigh of relief after closing, only to realize their wallets are about to take another hit. Hidden behind the paperwork and celebration, post-closing costs lurk in the background. These aren’t just minor annoyances—they can chip away at your budget if you don’t plan ahead. Let’s spotlight two big expense categories almost everyone underestimates: moving and immediate repairs, plus those easy-to-miss extra protection plans.

Photo by Ketut Subiyanto

Photo by Ketut Subiyanto

You’ve closed, the house is yours, but now reality sets in—moving is expensive. Most people budget for the actual move itself, but the costs don’t stop with the moving truck.

Here’s what often gets missed:

Many buyers and sellers are wiped out by these costs because they’re often overlooked in the home stretch. If your budget is tight, even a couple of unplanned repairs can throw off your plans and delay settling in.

The thrill of a new home quickly fades if a major system fails right after move-in. Home warranties and service contracts sound optional, but they deliver real comfort—if you actually budget for them.

What to watch out for:

Smart buyers weigh the price against what’s already covered by homeowners insurance and set aside a buffer for unexpected breakdowns. Sellers, on the other hand, may use a warranty as a bargaining chip but rarely account for adding it into their bottom-line costs.

Skipping this line item in your moving budget may leave you one broken water heater away from scrambling for emergency cash. A little planning means you’re not left cold—literally or financially—after the deal is done.

Title company charges at closing typically include a title search fee ($150–$500), title insurance for the lender and optionally for yourself as the buyer (each 0.5%–1% of the sale price), recording fees ($50–$300), and a settlement or escrow fee ($1,000–$2,500). Transfer taxes may also apply depending on your location. Use our free rate calculator to get an accurate estimate for your PA or NJ transaction.

A title settlement fee — sometimes called a closing fee or escrow fee — is what the title company charges to coordinate and conduct your closing. It covers document preparation, fund collection and disbursement, signatures, and the neutral third-party oversight needed to transfer ownership cleanly. At Pride Abstract, our settlement process covers everything from order entry through post-settlement recording.

At closing, a title company typically charges a settlement or escrow fee ($1,000–$2,500), a title search fee ($150–$500), title insurance premiums (0.5%–1% of sale price for each policy), recording fees ($50–$300), and applicable transfer taxes. For sellers, a title insurance policy paid on the buyer’s behalf may run $1,000–$3,000 depending on the market.

A title company earns revenue from the settlement fee, title search, and insurance premiums — not from a percentage commission on the sale price. Total title company revenue per closing varies based on the services provided and your property’s sale price. Use our rate calculator to see a detailed estimate for your specific transaction.

In Pennsylvania, the buyer traditionally pays title insurance and title search costs and therefore has the legal right to select the title company. Under federal law, if you are using a federally-related mortgage to purchase a primary residence, a seller cannot require you to use a specific title company unless the seller pays 100% of the insurance fees. In PA, you always have the right to choose your own title company. Know Your Rights as a homebuyer in PA

Title insurance protects against four hidden risks: errors in public records (incorrect names, signatures, or legal descriptions in deeds); judgments, liens, and unpaid mortgages that become the new owner’s responsibility; claims to ownership by a former owner, spouse, or missing heir; and invalid deeds from previous sellers who did not actually own the property or lacked legal capacity. Both lender and owner policies are available — only the owner’s policy protects your investment directly.

If you’re buying or selling in Pennsylvania or New Jersey, your title company charges follow state-specific rules and processes that differ from national norms. Knowing who has the right to choose the title company — and what fees to expect — gives you a real advantage at the closing table.

In Pennsylvania, the buyer traditionally pays title insurance and title search costs — which means the buyer has the legal right to select the title company. That’s important: it means you are not required to use whichever company your agent, lender, or seller prefers.

Pride Abstract & Settlement Services handles the full settlement process across PA and NJ — from title search and insurance to fund disbursement and post-settlement recording. Our rate calculator gives you an instant, accurate estimate of your title fees based on your specific sale price and location.

Veterans, first-time buyers, realtors, and investors all have questions specific to their situation — and our team has the local expertise to answer them. Reach out to the Pride Abstract office nearest to you or use our free rate calculator to get started.

Closing day doesn’t have to feel like a maze of surprise charges. Knowing where overlooked fees usually hide gives you the power to plan ahead and keep more money in your pocket.

Start by reviewing every closing estimate line by line. Ask your lender and agent to explain small admin fees, taxes, and charges you don’t recognize—no question is too basic. If you’re buying or selling in Pennsylvania, our title insurance calculator PA gives you an accurate rate estimate before you even sit down at the table.

Compare quotes for services like title insurance or inspections; you can often save by shopping around. Always confirm what falls to buyers, what belongs to sellers, and what’s split.

Set aside extra funds for moving, quick repairs, and the first months of taxes or insurance, so your budget stays on track after the dust settles. The more time you spend upfront understanding costs, the fewer surprises you’ll face later.

Thanks for reading—share your own closing stories or extra tips below to help others stay a step ahead. A little awareness now can save you stress, time, and thousands of dollars when it matters most.

Don’t let surprise fees catch you off guard. Contact the Pride Abstract team today and let our PA & NJ settlement experts guide you through every step of the closing process.

Last Update : February 2026